Identity theft is defined as the unauthorized use of your personal information to commit fraud, and the warning signs often appear weeks or months before you realize anything is wrong. Most people miss the early indicators because they look minor: a small unfamiliar charge, a piece of mail that never arrived, or a password reset email you never requested. Identity theft frequently goes unnoticed because thieves with direct access to your data can bypass standard defenses entirely. Knowing what to look for puts you back in control before the damage compounds. This guide walks you through the specific warning signs, the monitoring tools that catch fraud early, and the exact steps to take when something feels off.

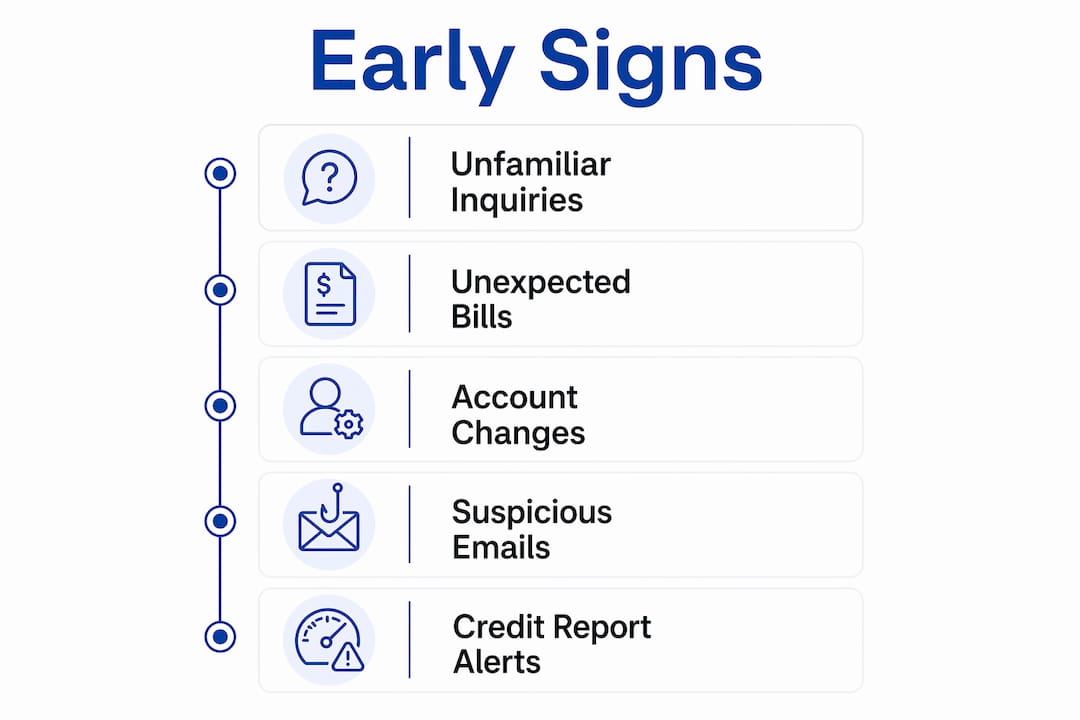

What are the most common early signs of identity theft?

The earliest indicators of identity fraud are easy to dismiss as errors. That is exactly what makes them dangerous. Recognizing these identity theft warning signs before they escalate is the difference between a quick fix and months of recovery.

Watch for these specific red flags:

- Unfamiliar accounts or credit inquiries. A new credit card or loan you never applied for appearing on your credit report is a direct signal that someone used your information.

- Unexpected bills or debt collection calls. Receiving a bill for an account you never opened means a creditor has already extended credit in your name.

- Emails for purchases or password resets you never initiated. Unrequested password reset emails indicate that someone is actively probing or has already accessed your account.

- Small unauthorized charges. Fraudsters make small purchases under $5 to confirm a card is active before running larger transactions. A $1.00 charge from an unknown vendor is not a glitch.

- Missing or rerouted mail. If your bank statements or tax forms stop arriving, a thief may have filed a fraudulent USPS change-of-address request. USPS sends a Move Validation Letter within 10 business days of any address change. Receiving one you never requested is a direct fraud signal.

- Medical bills for care you never received. Medical bills or statements for unreceived care reveal that someone used your insurance or identity to obtain medical services.

- Unrequested multi-factor authentication prompts. A login alert or MFA code arriving on your phone when you are not signing in means someone else is attempting access.

- Unexpected IRS notices. A notice about a duplicate tax return or income from an employer you do not recognize signals tax-related identity fraud.

Pro Tip: Set up text or email alerts on every bank and credit card account you own. Most financial institutions offer this for free, and a real-time alert on a $0.99 charge is far easier to dispute than a pattern discovered three months later.

How to use credit reports and digital tools to detect fraud early

Monitoring your credit and digital footprint is the most reliable method for catching identity fraud before it becomes a crisis. The tools available today are free, accessible, and genuinely effective when used consistently.

Pull reports from all four major credit bureaus

You can access free weekly credit reports from Experian, Equifax, TransUnion, and Innovis at AnnualCreditReport.com. Most people check only the three major bureaus and skip Innovis entirely. That gap matters because Innovis is used for secondary verification by lenders and mailers, and a freeze there closes a real vulnerability.

When reviewing each report, check for:

- Credit accounts you never opened

- Lender inquiries from companies you never contacted

- Addresses listed that you have never lived at

- Employers listed that you have never worked for

Use digital monitoring and breach detection

| Tool | What it detects | Cost |

|---|---|---|

| AnnualCreditReport.com | New accounts, inquiries, address changes | Free |

| HaveIBeenPwned | Email addresses exposed in data breaches | Free |

| Experian credit monitoring | Daily credit changes, dark web scanning | Free tier available |

| IRS IP PIN program | Fraudulent tax filings in your name | Free |

HaveIBeenPwned lets you enter your email address and see every known data breach that exposed it. If your email appears in a breach, change that password immediately and check every account that uses the same credentials.

The IRS Identity Protection PIN is a six-digit code that prevents anyone from filing a tax return using your Social Security number without it. You can enroll at irs.gov/ippin. This single step blocks one of the most financially damaging forms of identity fraud.

Pro Tip: Stagger your credit report pulls across the four bureaus, checking one every few weeks instead of all four at once. This gives you near-continuous coverage throughout the year rather than one snapshot.

For creators and individuals with a significant online presence, social media identity fraud adds another layer of exposure that standard credit monitoring does not cover. Pairing credit monitoring with digital identity scanning closes that gap. Using biometric authentication on mobile apps also reduces the risk of account takeover, which is one of the fastest-growing vectors for identity fraud.

What to do immediately when you spot early warning signs

Speed matters. The faster you act on the early signs of identity fraud, the less damage a thief can do. Work through these steps in order.

- Contact the company directly. Call the financial institution or creditor listed on the unfamiliar account using a verified phone number from their official website. Do not use contact information from the suspicious bill itself.

- File a report at IdentityTheft.gov. Reporting to IdentityTheft.gov generates a personalized federal recovery plan and pre-filled dispute letters. This is the fastest path to a structured response.

- Place fraud alerts or credit freezes. Contact all four bureaus, including Innovis, to place a fraud alert or freeze. A freeze prevents new credit from being opened in your name entirely.

- Set up an IRS Identity Protection PIN. Enroll at irs.gov/ippin if you have not already. This blocks fraudulent tax filings immediately.

- Document everything. Save copies of every suspicious bill, email, and notification. Screenshot account activity. This evidence supports your disputes and any law enforcement reports.

- Change compromised passwords immediately. Use a unique, strong password for every account. Enable two-factor authentication on all financial, email, and social accounts.

- File a police report if a creditor requires it for dispute resolution.

- Notify your health insurer if you suspect medical identity theft.

- Monitor your credit reports weekly for the next 90 days after detecting fraud.

- Consider enrolling in a digital identity protection service for ongoing monitoring beyond the initial response.

Confirming identity theft quickly and using IdentityTheft.gov produces a faster, more organized recovery. Delay is the single biggest factor that turns a manageable situation into a prolonged financial and legal problem.

Common mistakes that let identity theft go undetected

Most people who discover identity theft months after the fact made at least one of these errors. Avoiding them is as important as knowing the warning signs.

- Ignoring small irregularities. A single unfamiliar $2.00 charge feels too minor to investigate. Thieves count on that reaction. Treat every unknown transaction as a signal worth checking.

- Pulling reports from only one or two bureaus. Each bureau holds independent data. Fraud that appears on a TransUnion report may not show on Experian yet. Check all four.

- Skipping Innovis. Failing to freeze credit with Innovis leaves a gap that many thieves exploit precisely because most people overlook this bureau.

- Ignoring missing mail. If your bank statement or a tax document stops arriving, do not assume a postal delay. Missing mail often results from fraudulent USPS address changes designed to intercept sensitive documents.

- Delaying reporting out of embarrassment. Identity theft is not a personal failure. Reporting it quickly to IdentityTheft.gov and your creditors limits the financial damage and creates a legal record.

Pro Tip: Review your Explanation of Benefits statements from your health insurer every time one arrives. Medical identity theft is one of the least-detected forms of fraud because people rarely scrutinize healthcare billing. A charge for a procedure you never had is a clear indicator.

Pro Tip: Enter your email address into HaveIBeenPwned at least once a quarter. If your credentials appear in a new breach, you will know before a thief uses them.

For a broader view of how your personal data gets exposed in the first place, understanding why personal info gets scraped online helps you reduce your attack surface proactively. Pair that awareness with advanced mobile security strategies to protect the accounts most vulnerable to takeover.

Key Takeaways

Early detection of identity fraud depends on consistent monitoring of credit reports, digital accounts, and physical mail, combined with fast action the moment a warning sign appears.

| Point | Details |

|---|---|

| Check all four credit bureaus | Pull reports from Experian, Equifax, TransUnion, and Innovis to catch fraud across every reporting channel. |

| Small charges are not accidents | A charge under $5 from an unknown source is a common test by fraudsters before larger transactions. |

| Missing mail is a fraud signal | A USPS Move Validation Letter you never requested means someone rerouted your mail to intercept documents. |

| IdentityTheft.gov speeds recovery | Filing there generates a federal recovery plan and pre-filled dispute letters to resolve fraud faster. |

| Freeze credit at all four bureaus | Including Innovis in your credit freeze closes a gap most people leave open without realizing it. |

What I have learned from watching identity theft unfold in silence

The most striking thing about identity theft is how quiet it is at the start. You do not get a notification that your data was stolen. You get a $1.47 charge on a Tuesday, a medical bill for a clinic you have never visited, or a tax notice that arrives in april for income you never earned. Each one feels like a clerical error. That is the design.

At Sidenty, we work with people who have already experienced the gut punch of discovering their identity was compromised. The pattern is almost always the same: the signs were there months earlier, and they were dismissed. A password reset email that seemed like a phishing attempt. A credit inquiry from an unfamiliar lender that seemed like a mistake. The people who catch fraud early are the ones who treat every anomaly as worth five minutes of investigation.

The tools exist. AnnualCreditReport.com, HaveIBeenPwned, the IRS IP PIN program, and real-time bank alerts cost nothing and take less than an hour to set up. The gap is not access. The gap is the habit of checking. Building that habit before you have a reason to is the single most effective thing you can do for your financial and digital security. Recognizing identity theft early is not about paranoia. It is about knowing what normal looks like so that anything abnormal stands out immediately.

— Sidenty

Sidenty’s approach to protecting your digital identity

Detecting the early signs of identity fraud is the first step. Staying protected after that requires ongoing monitoring that most people cannot maintain alone.

Sidenty provides professional digital identity protection built for people who take their online presence seriously. With AI-powered scanning, real-time alerts, and a team of legal experts, Sidenty monitors your digital identity across platforms and acts fast when something goes wrong. The digital identity protection services at Sidenty carry a 99.8% success rate in content removal and cover threats ranging from unauthorized account use to deepfake creation. If you are concerned about your exposure, Sidenty’s anti-piracy and identity monitoring tools give you professional-grade coverage without requiring you to manage it yourself.

FAQ

What are the first signs of identity theft?

The earliest signs include unfamiliar credit inquiries, unexpected bills for accounts you never opened, small unauthorized charges, and password reset emails you never requested. Missing mail or a USPS Move Validation Letter you did not initiate is also a direct early warning.

How do I check if my identity has been stolen?

Pull free weekly credit reports from all four major bureaus at AnnualCreditReport.com and review them for unknown accounts, addresses, and inquiries. Also check your email address on HaveIBeenPwned to see if your credentials appeared in a known data breach.

What should I do first if I suspect identity theft?

Contact the company involved using a verified phone number, then file a report at IdentityTheft.gov to receive a personalized federal recovery plan. Place a credit freeze with all four bureaus, including Innovis, and change the passwords on any compromised accounts immediately.

What is an IRS Identity Protection PIN and do I need one?

An IRS Identity Protection PIN is a six-digit code that prevents anyone from filing a tax return using your Social Security number without it. Enrolling at irs.gov/ippin is free and blocks one of the most financially damaging forms of identity fraud.

Can identity theft happen from someone I know?

Yes. Familiar fraud, where a known person misuses your personal data, is a common and often silent form of identity theft. It bypasses phishing defenses because the perpetrator already has direct access to your information.